Public Investment, Construction Demand, and Risk Management Fuel Strong Performance

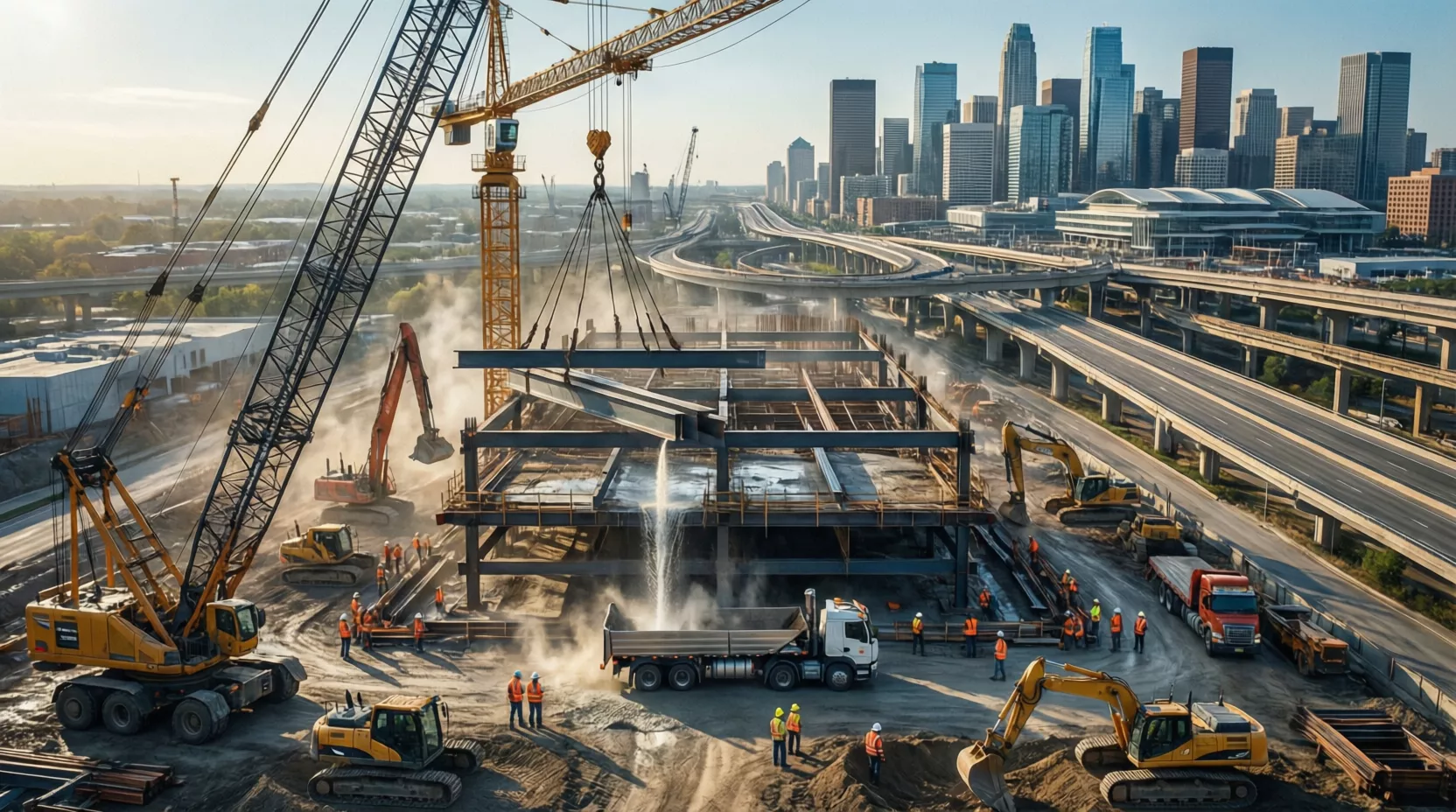

Federally funded infrastructure initiatives continue to play a pivotal role in driving premium growth and profitability for U.S. surety bond writers, according to a new report from AM Best. The construction-focused line of business has now generated underwriting profits exceeding $2 billion for a third consecutive year in 2024, underscoring the sector’s sustained strength amid elevated public and private investment activity.A major contributor to this momentum remains the Infrastructure Investment and Jobs Act of 2021 (IIJA), which has significantly boosted public construction spending across the United States. As a result, surety insurers have experienced strong premium growth tied to federally funded projects. AM Best reports that direct written premium through the first nine months of 2025 increased by nearly 10% compared with the same period in 2024, reflecting continued demand for bonding capacity in public infrastructure development.

While IIJA-related funding has provided a substantial tailwind, the report cautions that this source of growth may begin to taper. The legislation is scheduled to expire in September 2026, and AM Best notes that the winding down of federal funding could lead to a slowdown in public construction spending unless additional legislation or alternative funding mechanisms are introduced.

Despite this potential headwind, the surety market is not solely dependent on traditional public infrastructure. Emerging areas of investment—particularly high-technology manufacturing facilities, data centers, and other large-scale capital expenditure projects—are increasingly creating new bonding opportunities. These projects, many of which are supported by reshoring initiatives, digital transformation, and energy transition efforts, often require complex surety arrangements.

As technologies become more advanced and insurers consider expansion opportunities in emerging risk areas, the build-out through additional projects may spur future premium growth attributable to public and private infrastructure initiatives over the near term,” said David Blades, associate director at AM Best. He added that these evolving construction needs could help offset any eventual decline in federally funded infrastructure work.

Notably, premium growth in the surety sector has remained strong even though pricing conditions have been relatively stable in recent years. This suggests that growth is being driven more by increased project volume and scale rather than rate hardening. The trend has persisted well into 2025, with underwriting profitability continuing to improve.

According to the report, the industry’s direct incurred loss ratio for surety business declined by more than four percentage points year-to-date through the third quarter of 2025, compared with the same period in 2024. The combination of higher premium volume and lower loss ratios positions surety insurers for a meaningful increase in bottom-line profitability for the full year.

Results through the first nine months of 2025 show both continued growth for surety insurers and favorable underwriting trends,” said Robert Valenta, senior financial analyst at AM Best. He noted that disciplined underwriting practices and favorable project performance have supported strong financial outcomes across the sector.

The long-term profitability of the surety line remains one of its most distinguishing characteristics. Surety insurers have produced net profit margins exceeding 30% in each of the past 11 years, from 2014 through 2024, according to AM Best. When compared with other major U.S. commercial insurance lines, surety has consistently outperformed its peers over that period.

However, the report also highlights a structural limitation. Despite its exceptional profitability, the surety line represents a relatively small share of overall U.S. property and casualty premium volume. As a result, its strong margins have only a modest impact on the broader industry’s aggregate profitability.

Even so, AM Best views the surety sector’s performance as a model of underwriting discipline and risk selection. As infrastructure investment evolves—shifting from traditional public works to advanced manufacturing, digital infrastructure, and private capital-driven projects—surety insurers appear well positioned to sustain growth and profitability in the near to medium term, even as federal funding dynamics change.